-

A HOUSE LOAN

A HOUSE LOAN

Terms of Credit

Every loan agreement specifies an interest rate which the borrower must pay to the lender along with the repayment of the principal. In addition, lenders may demand collateral (security) against loans. Collateral is an asset that the borrower owns (such as land, building, vehicle, livestock, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid. If the borrower fails to repay the loan, the lender has the right to sell the asset or collateral to obtain payment. Property such as land titles, deposits with banks, livestock are some common examples of collateral used for borrowing

Interest rate, collateral and documentation requirement, and the mode of repayment together comprise what is called the terms of credit. The terms of credit vary substantially from one credit arrangement to another. They may vary depending on the nature of the lender and the borrower. The next section will provide examples of the varying terms of credit in different credit arrangements.

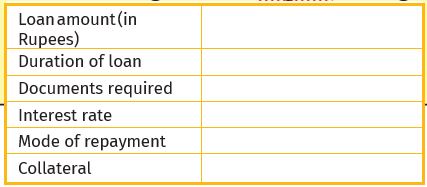

Megha has taken a loan of Rs 5 lakhs from the bank to purchase a house. The annual interest rate on the loan is 12 percent and the loan is to be repaid in 10 years in monthly installments. Megha had to submit to the bank, documents showing her employment records and salary before the bank agreed to give her the loan. The bank retained as collateral the papers of the new house, which will be returned to Megha only when she repays the entire loan with interest.

Activity:

Fill in the following details of Megha’s housing loan.

Let’s work these out

1. Why do lenders ask for collateral while lending?

2. Given that a large number of people in our country are poor, does it in any way affect their capacity to borrow?

3. Fill in the blanks choosing the correct option from the brackets.

While taking a loan, borrowers look for easy terms of credit. This means (low/high) interest rate, (easy/ tough) conditions for repayment, (less/more) collateral and documentation requirements.

Source: This topic is taken from NCERT TEXTBOOK

-

VARIETY OF CREDIT ARRANGEMENTS

VARIETY OF CREDIT ARRANGEMENTS

Example of a Village

Rohit and Ranjan had finished reading about the terms of credit in the class. They were eager to know the various credit arrangements that existed in their area: who were the people who provided credit? Who were the borrowers? What were the terms of credit? They decided to talk to some people in their village. Read what they record.

15th Nov 2019.

We head directly for the fields where most farmers and labourers would be working at this time of the day. The fields are planted with potato crops. We first met Shyamal, a small farmer in Sonpur, a small irrigated village.Shyamal tells us that every season he needs loans for cultivation on his 1.5 acres of land. Till a few years back, he would borrow money from the village moneylender at an interest rate of five percent per month (60% per annum). For the last few years, Shyamal has been borrowing from an agricultural trader in the village at an interest rate of three percent per month. At the beginning of the cropping season, the trader supplies the farm inputs on credit, which is to be repaid when the crops are ready for harvest.

Besides the interest charge on the loan, the trader also makes the farmers promise to sell the crop to him. This way the trader can ensure that the money is repaid promptly. Also, since the crop prices are low after the harvest, the trader is able to make a profit from buying the crop at a low price from the farmers and then selling it later when the price has risen.

We next meet Arun who is supervising the work of one farm labourer. Arun has seven acres of land. He is one of the few persons in Sonpur to receive bank loans for cultivation. The interest rate on the loan is 8.5 percent per annum and can be repaid anytime in the next three years. Arun plans to repay the loan after harvest by selling a part of the crop. He then intends to store the rest of the potatoes in cold storage and apply for a fresh loan from the bank against the cold storage receipt. The bank offers this facility to farmers who have taken crop loans from them.

Rama is working in a neighbouring field. She works as an agricultural labourer. There are several months in the year when Rama has no work and needs credit to meet the daily expenses. Expenses on sudden illnesses or functions in the family are also met through loans. Rama has to depend on her employer, a medium landowner in Sonpur, for credit. The landowner charges an interest rate of 5 percent per month. Rama repays the money by working for the landowner. Most of the time, Rama has to take a fresh loan, before the previous loan has been repaid. At present, she owes the landowner Rs 5,000. Though the landowner doesn’t treat her well, she continues to work for him since she can get loans from him when in need. Rama tells us that the only source of credit for the landless people in Sonpur is landowner-employers.

Let’s work these out

1. List the various sources of credit in Sonpur.

2. Underline the various uses of credit in Sonpur in the above passages.

3. Compare the terms of credit for the small farmer, the medium farmer and the landless agricultural worker in Sonpur.

4. Why will Arun have a higher income from cultivation compared to Shyamal?

5. Can everyone in Sonpur get credit at a cheap rate? Who are the people who can?

6. Tick the correct answer.

(i) Over the years, Rama’s debt.

(a) will rise.

(b) will remain constant.

(c) will decline.

(ii) Arun is one of the few people in Sonpur to take a bank loan because.

(a) other people in the village prefer to borrow from the moneylenders.

(b) banks demand collateral which everyone cannot provide

(c) interest rate on bank loans is the same as the interest rate charged by the traders.

7. Talk to some people to find out the credit arrangements that exist in your area. Record your conversation. Note the differences in the terms of credit across people.

Source: This topic is taken from NCERT TEXTBOOK

-

LOANS FROM COOPERATIVES

LOANS FROM COOPERATIVES

Besides banks, the other major source of cheap credit in rural areas are the cooperative societies (or cooperatives). Members of a cooperative pool their resources for cooperation in certain areas. There are several types of cooperatives possible such as farmers cooperatives, weavers cooperatives, industrial workers cooperatives, etc. Krishak Cooperative functions in a village not very far away from Sonpur. It has 2300 farmers as members. It accepts deposits from its members. With these deposits as collateral, the Cooperative has obtained a large loan from the bank. These funds are used to provide loans to members. Once these loans are repaid, another round of lending can take place.

Krishak Cooperative provides loans for the purchase of agricultural implements, loans for cultivation and agricultural trade, fishery loans, loans for construction of houses and for a variety of other expenses.

Source: This topic is taken from NCERT TEXTBOOK